There is something to be said about people who have been seriously contemplating their future–and been looking at what is life insurance about.

Life insurance offers financial security and protection to the beneficiaries in the event of the policyholder’s death. The benefits can also be used to cover expenses such as funeral costs, outstanding debts, mortgages, or to provide a source of income for the surviving family members.

If you are one of the many who hadn’t thought about financial security but changed their mind, read on to know what is life insurance and its high potential to help you and your family.

Key Takeaways 💡🌞

- Life insurance is a contract – and a legally binding one – that pays a death benefit to the insured person’s beneficiaries at the time of their passing.

- For a life insurance policy to remain in effect, the policyholder is required to pay upfront a single premium, or pay regular premiums until its completion.

- Upon the policyholder’s death, the named beneficiaries will receive the policy’s death benefit.

- Term life insurance policies expire after a specific period of years. On the other hand, Permanent life insurance policies remain active until premium payments stop, surrender the policy, or until the policyholder’s death.

- A life insurance policy is only deemed as effective as the insurance company’s financial strength. However, if the insurance company cannot issue payments anymore, State guaranty funds may pay claims to the policyholder.

What Is Life Insurance Policy

Getting to know what is a life insurance policy shouldn’t pose any difficulty as long as you take the time to review and make changes if necessary.

Below are the common life insurance terms:

Premium

A Premium Life Insurance policy offers coverage in exchange for the payment of a regular premium. This can be paid either on a monthly, quarterly, semi-annual, or annual basis, and the policy remains in effect as long as the premium payments are up-to-date.

Death Benefit

The death benefit is the main reason many individuals opt to buy life insurance because it helps provide financial support to the policyholder’s loved ones in the event of their demise.

Cash Value

In buying life insurance, the policy’s cash value component is invested and grows over the years. The funds can be accessed through loans or withdrawals.

Policy Length

The length of a life insurance policy will depend on the individual’s specific needs and financial situation. As such, policies can have varying terms and lengths, ranging from annual terms to a whole lifetime.

What Are The Different Types of Life Insurance?

There are two main types of life insurance: permanent life insurance, and term life insurance. Within these two categories, there are several subtypes of life insurance policies.

Term Life Insurance

This is the simplest and most affordable type of life insurance. It provides coverage for a specified term, usually ranging from 1 to 30 years, and pays a death benefit only if the policyholder dies within the term.

Permanent Life Insurance

Permanent life insurance, also known as whole life insurance, is a type of life insurance policy that provides coverage for the insured’s entire lifetime, as long as the premiums are paid.

Whole Life

Whole life insurance (also known as permanent life insurance) includes a savings component known as the cash value. The policy’s cash value can increase through the years, and policyholders can borrow against it or access it in other ways, depending on the policy’s terms.

Read More: Term vs Whole Life Insurance

Universal Life

Universal life insurance offers both insurance protection and a tax-deferred investment component. It affords policyholders greater flexibility than traditional whole life insurance, as they have the ability to adjust their death benefit, premium payments, and investment advantages and choices within certain limits.

Variable Life Insurance

With Variable life insurance, this one combines elements of both traditional life insurance and investment opportunities. Unlike traditional life insurance policies that come with a guaranteed death benefit, variable life insurance’s policy is volatile and can fluctuate based on the performance of the underlying investments.

Read More: Term vs Whole Life Insurance

What Impacts the Cost of Your Life Insurance?

Of course, part of what is life insurance about are listed below—the known reasons that can impact the cost of your life insurance:

- Age – Generally, the younger you are when you purchase life insurance, the lower your premiums will be.

- Health – If you have pre-existing health conditions, it can impact the cost of your life insurance, as the insurer views you as a higher risk

- Location – The cost of life insurance can also vary based on where you live, as certain regions may have higher rates of certain health issues or natural disasters.

- Coverage amount – The amount of coverage you choose will also impact the cost of your life insurance. Higher coverage amounts generally result in higher premiums.

- Term length – The length of the term for which you purchase life insurance can also impact the cost. Shorter term lengths generally result in lower premiums, while longer term lengths result in higher premiums.

- Smoking status – Smokers generally pay higher premiums for life insurance, as they are at a higher risk for certain health issues.

- Occupation and hobbies – Certain occupations and hobbies, such as being a pilot or skydiving, can result in higher premiums, as they are considered higher-risk.

Age

The older a person is, the more expensive their life insurance policy will be, because they are considered to be at a higher risk of death.

Gender

In general, women tend to live longer than men and are therefore considered to be lower risk, which can result in lower life insurance premiums.

Health

If an individual has a pre-existing medical condition or a history of serious health issues, they may be deemed a high- risk candidate to the insurance company.

As a result, they may be offered lower coverage amounts or higher premiums. On the other hand, if an individual is in good health, they may be able to secure a higher coverage amount for a lower premium.

Lifestyle Choices

Life insurance companies assess the level of risk associated with insuring someone based on a variety of factors, including their lifestyle choices. Some lifestyle choices, such as smoking or engaging in hazardous activities, can increase the risk of death, which in turn can increase the cost of life insurance.

| Gender | When Buying Life Insurance | Lifestyle Factors That Can Have Direct Impact On Life Insurance |

| Female | Women generally pay more for life insurance premiums than women who are not insured. | Obesity, alcohol intake, smoking and/or vaping habits, engaging in extreme sports and hobbies, age, medical history (also from family), occupation/trade, other medical conditions. |

| Male | Men tend to sign up late to get insurance, and pay premiums accordingly than men who are not insured. | Alcohol intake, smoking and/or vaping habits, engaging in extreme sports and hobbies, diet and fitness, medical conditions and history (also including family history), driving record, occupation/trade. |

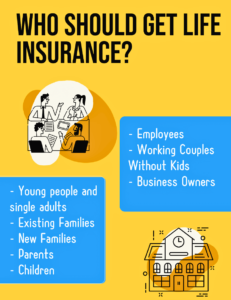

Who Should Get Life Insurance?

Life insurance is an important consideration for anyone, regardless of their age or relationship status. If you or know anyone who has been thinking what is life insurance and have become very interested in signing up, next are the types of people who need to have life insurance:

Young People and Single Adults

The main purpose of life insurance for this demographic is to provide financial security for the future, including covering end-of-life expenses and ensuring that their loved ones are financially protected in case of their untimely death.

Young and single adults typically have lower life insurance premiums compared to older individuals or those who are married and have dependents, due to the lower perceived risk associated with their age and lifestyle.

Existing Families

Having a life insurance policy in place helps families to maintain their standard of living and cover expenses, such as mortgage payments, education costs, and day-to-day living expenses, even the primary breadwinner passes away.

It also helps to provide financial stability and peace of mind, knowing that their loved ones will be taken care of if the worst were to happen.

New Families

What is life insurance for a new family? Certainly, being insured can definitely help maintain their standard of living and provide for their financial needs, such as paying for household expenses, education costs, and medical bills.

Parents

Life insurance is an important consideration for parents as it places importance in financial security for their dependents in the event of their untimely death.

Being insured does help cover expenses such as funeral costs, outstanding debts, and daily living expenses, as well as provide a source of income for the surviving family. Once the premiums are paid, it can also serve as a way to provide for children’s education or other long-term goals.

Children

By buying a life insurance policy when the child is young, they can lock in a lower premium rate that will remain in effect for the duration of the policy. This can be especially important for children who may have health issues that could make it difficult or expensive to obtain coverage later in life.

Individuals With Home Loans

Many people opt for life insurance that can help repay the outstanding mortgage balance in case of the policyholder’s death, providing financial security for their loved ones and protecting their home from being foreclosed. This also ensures that their families will not be forced to sell their home or downsize to make ends meet, preserving the assets that they have worked so hard to build.

Employees

Unfortunately, many employees have little to no knowledge of what is life insurance.

For many companies, life insurance serves as a valuable employee benefit that can attract and retain top talent, as it shows the employer’s commitment to their well-being and that of their families.

Working Couples Without Kids

Working couples without kids are often the main providers for each other and life insurance can provide financial protection for their partner in the event of their unexpected death.

Business Owners

A life insurance policy can also be used as a tool for business succession planning, providing funds for the transfer of ownership or to buy out a partner’s share. This can help maintain the stability and continuity of the business.

Families with children

Life insurance is designed to provide financial protection for your loved ones in the event of your death. If you have a family, especially children, having a life insurance policy can help ensure their future financial stability.

Inheritance

For many low-income families, investing in a long-term financial product paid out to their loved ones is what is life insurance about.

Life insurance can be an effective way to pass on inheritance to your beneficiaries. When you purchase a life insurance policy, you nominate a beneficiary or beneficiaries who will receive the death benefit if you pass away. The death benefit is a lump sum of money that is paid out tax-free to the beneficiaries.

Funeral Expenses

Final/funeral expense is known as Burial insurance, is a whole life policy that provides coverage for the individual’s final expenses. It pays for costs such as the casket or urn, memorial service, and cremation or burial.

Mortgage and Loans

Mortgage insurance is a type of life insurance policy that pays off the remaining mortgage balance in the event of the borrower’s death. On the other hand, Loan life insurance is similar to mortgage life insurance, but it is designed to cover other types of loans, such as personal loans or auto loans.

If Your Spouse Stays at Home

A stay-at-home spouse (either the husband or wife) will definitely require coverage so that, at the time of their demise, the surviving spouse could protect their earnings potential while also paying for services for the upkeep and maintenance of their home.

Life Insurance For Seniors

What is life insurance for seniors? Senior citizens too can enjoy the benefits of life insurance, and for older folk who are over the age of 60 or 65.

These policies offer financial protection for the senior’s beneficiaries in the event of their passing, ensuring that their loved ones are provided for financially even after they are gone.

The most suitable types of life insurance policies available for seniors are term life insurance, whole life insurance, and final expense insurance.

The type of policy that is best for the elderly will depend on their specific needs and financial situation. It is important for seniors to carefully consider their options and work with a trusted insurance agent to choose the policy that is right for them.

Read More: LIRP: A Life Insurance Tax-Free Retirement Plan

Beneficiaries

When you buy a life insurance policy, you can name a beneficiary or two.

What is a Beneficiary?

A beneficiary is a person or persons who are your recipients as the policyholder. The beneficiary will receive the death benefit from life insurance policy at the time of your passing.

Read more: What is Beneficiary

How can they make a claim for life insurance?

To make a beneficiary claim on a life insurance policy, the following steps can be taken:

- Obtain a death certificate – This will be required by the insurance company to prove the death of the insured person.

- Contact the insurance company – Get in touch with the life insurance company as soon as possible to notify them of the death. You can do this by phone, email, or in person.

- Have all the necessary information ready – The insurance company will need information such as the policy number, the date of death, and the name and contact information of the beneficiary. They may also ask for a copy of the death certificate and other supporting documentation.

- Fill out claim forms – The insurance company will provide you with the necessary claim forms that you need to fill out and return. Make sure that you provide all the required information and sign the forms as required.

- Wait for the processing of the claim – The insurance company will process the claim and determine the amount that is payable to the beneficiary. This process can take several weeks, and the insurance company will keep you updated on the status of your claim.

- Receive the payment – Once the claim has been approved and processed, the insurance company will send the payment to the beneficiary. This can be done by check, direct deposit, or wire transfer, depending on the terms of the policy and the preference of the beneficiary.

How Much Coverage Will I Need?

You have also thought not only about what is life insurance, but also the coverage. The coverage you will need will definitely depend on your situation: personal and financial circumstances, health status, dependents, and long-term financial goals.

Below are some of the determining components on how much life insurance you need:

- Income Replacement – This is the amount of money you need to replace your income if you were to pass away. It should cover your family’s living expenses and help maintain their standard of living.

- Debts and Liabilities – Consider any debts, such as mortgages, car loans, credit card debt, etc. that you would want to be paid off in the event of your death.

- Future Expenses – Think about future expenses such as your children’s education, weddings, etc.

- Estate Planning – If you want to leave an inheritance for your beneficiaries, life insurance can be an important component of your estate plan.

A general rule of thumb is to purchase a life insurance policy that is equal to 10 to 12 times your annual income.

However, this is just a starting point, and you may need more or less coverage depending on your specific circumstances.

It’s a good idea to consult with a financial advisor to get a good understanding about the amount of life insurance coverage that’s perfect for you.

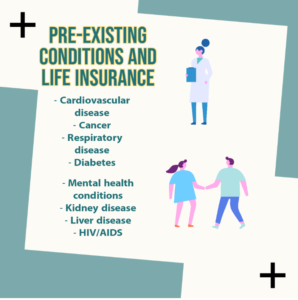

What Is Life Insurance Pre-existing Conditions

Common pre-existing conditions that can affect a person’s ability to get life insurance include:

- Cardiovascular disease – This includes conditions such as heart attack, stroke, and angina.

- Cancer – Life insurance companies will typically consider the type and stage of cancer, and how long it has been since treatment was completed.

- Respiratory disease – This includes conditions such as chronic obstructive pulmonary disease (COPD) and asthma.

- Diabetes – Life insurance companies will consider factors such as the type of diabetes, how well it is controlled, and any complications.

- Mental health conditions – This includes conditions such as depression, anxiety, and bipolar disorder.

- Kidney disease – Life insurance companies will consider factors such as the stage of the disease and whether the person is on dialysis.

- Liver disease – Life insurance companies will consider factors such as the stage of the disease and whether the person has liver cirrhosis.

- HIV/AIDS – Life insurance companies will consider factors such as the stage of the disease and the person’s overall health.

Some insurance companies may also have different underwriting guidelines for specific conditions.

How To Purchase Life Insurance

Knowing more about what is life insurance, how much would it be, and finally purchasing it can be an easy task if you carefully follow these steps:

- Ensure your coverage needs – Consider factors such as your age, current income, and debts, to determine the amount of coverage you need. It’s important to choose a coverage amount that will provide financial stability for your family in the event of your death.

- Look for, and compare different life insurance policies – There are two main types of life insurance policies: term life insurance and whole life insurance. Consider the features and benefits of each policy and compare quotes from different insurance companies to find the best policy for you.

- Consider your budget – When choosing a policy, consider how much you can afford to pay for premiums each month. You should also consider the length of the policy, as longer policies will generally have higher premiums.

- Search, review, and choose an insurance company that can meet your needs – Research the insurance company’s financial stability and customer satisfaction ratings. You can do this by checking with the National Association of Insurance Commissioners (NAIC) or by reading online reviews.

- Fill out an application – Once you have chosen a policy, you will need to fill out an application. You will likely be asked to provide information such as your age, occupation, health history, and lifestyle.

- Undergo a medical exam (if required) – Some life insurance policies require a medical exam, while others do not. If a medical exam is required, a representative from the insurance company will come to your home or workplace to conduct the exam.

- Pay your premiums – Once your application has been approved and your policy has been issued, you will need to pay your premiums on time to keep your coverage in force.

Questions To Ask Your Life Insurance Agent

If you have been considering buying life insurance, naturally there are some questions that you have—and this is perfectly okay.

Here are the most important questions that you can ask your agent:

- What types of life insurance policies do you offer?

- Can you explain the differences between term and permanent life insurance?

- How does the application and underwriting process work?

- What factors determine the premium amount for a life insurance policy?

- How can I make changes to my existing policy, if needed?

It’s highly recommended that you first consult with an agent to help you find a good policy that will match your specific situation which will no doubt play a major role in getting the best life insurance.

Frequently Asked Questions

What Is Life Insurance and How Does It Work?

Life insurance is a financial agreement between an individual (the policyholder) and an insurance company. The policyholder pays a premium in exchange for the insurance company’s promise to pay a lump sum benefit to the designated beneficiaries in the event of the policyholder’s passing.

How Much is Life Insurance?

The cost of life insurance depends on several factors such as the policyholder’s age, health, coverage amount, and term length.

For example, a healthy 30-year-old who wants a 20-year term life insurance policy with a $500,000 death benefit might pay an average monthly premium of $25. But then again, the cost can be much higher or lower depending on the individual’s circumstances.

It should be noted that looking for insurance companies and understanding their policies, coverage, and quotes to find the best policy for your budget and needs.

It’s also worth keeping in mind that life insurance premiums can increase over time, so it’s a good idea to review your coverage regularly and make adjustments as needed.

What is life insurance death benefit?

A death benefit is a payment made to the beneficiaries of a deceased person, mainly as a result of that person having had an insurance policy or an investment product, such as life insurance.

The death benefit is intended to give out financial support to the beneficiaries in the event of the policyholder’s death.

Are life insurance payouts tax-free?

In most cases, yes, life insurance payouts are tax-free to the beneficiary. In the United States, death benefits from a life insurance policy are generally not considered taxable income.

This means that the beneficiary does not have to pay federal or state income tax on the death benefit received from the life insurance policy.

Can I buy life insurance if I have a pre-existing condition?

Yes, you can buy life insurance even if you have a pre-existing medical condition. But, the availability and cost of coverage may differ based on your condition.

What is life insurance rider?

A life insurance rider is a provision or an add-on feature to a life insurance policy that provides additional coverage or benefits. It allows policyholders to customize their life insurance policies to meet their specific needs and circumstances.

What are the benefits of life insurance?

Not only does life insurance give out payouts to the policyholder’s beneficiaries upon their passing but it also helps keep loved ones afloat financially. It’s also an investment on its own, where the principal amount grows within a specific timeframe.

Can I inherit from life insurance?

As with most types of life insurance policies, premiums need to be fully paid which can grow through the years, and can act as inheritance if and when the insured passes away.

If you’re the sole beneficiary or one of the listed beneficiaries in the policyholder’s insurance, ultimately, you’ll be able to file a claim for the insured amount.

Can I use my life insurance for when I or a family member gets ill?

Yes, actually you can use life insurance while alive in various ways. Just make sure the premiums are being paid regularly beforehand and without late/staggering payments. Contact your life insurance company or the agent for assistance in filing a claim.

How do I choose the right life insurance policy for me?

- Determine your coverage needs by considering factors such as dependents, outstanding debts, and future financial goals.

- Evaluate different policy types, such as term or permanent life insurance, to know and understand which best suits your needs and budget.

- Compare quotes from multiple insurance companies to find the best combination of coverage, cost, and customer service.

To Wrap Up

The purpose of life insurance is to maintain financial security and peace of mind for the policy holder’s loved ones and dependents in the event of their death.

There are different types of life insurance policies, including term life insurance, whole life insurance, and universal life insurance. When obtaining life insurance, the policyholder pays a premium either in a lump sum or in instalments. One should familiarise themselves with the various life insurance policies available, determine what sort of coverage they require and factor in their budget prior to purchasing a policy.

Sources

Insurancereviews.org follows stringent sourcing guidelines by utilizing peer-reviewed studies, academic research institutions, and industry associations to ensure the reliability and accuracy of our content. We refrain from using tertiary references and prioritize primary sources. To learn more about our commitment to delivering up-to-date and accurate information, please refer to our editorial policy.

- https://www.investopedia.com/terms/l/lifeinsurance.asp – April 2023

- https://www.iciciprulife.com/insurance-library/insurance-basics/what-is-life-insurance.html – April 2023

- https://en.wikipedia.org/wiki/Life_insurance – April 2023